This post may contain affiliate links (including amazon.com because we participate in the Amazon Services LLC Associates Program). Full disclosure is here.

Credit card debt, car loans, student loan debt, personal loans, you name it – debt can lead to a lot of stress. Want to know how to manage and pay off all your debt? There is a solution: the debt snowball method. Here’s a free debt snowball worksheet to take you from drowning in debt to debt free in four easy steps. Plus, there’s a visual debt payment tracker to keep creatives motivated!

If you owe money then you’re certainly not alone.

Did you know that most Americans owe $38 000 in personal debt, with 2 in 10 spending 50-100% of their income on paying off debt? In fact, a 2016 study found that the average American household owes $16 000 on their credit cards alone. According to the US Census Bureau, the average annual household income in 2017 was $61 372, meaning that the average household debt is more than half their average annual income.

I’ve been proudly debt-free since 2016. That’s years of good sleep and no stress when the bills come in. No nasty surprises. No bad debt. And no bad credit ratings.

There’s really no big secret to my success. I did it with the debt snowball method, which is today’s fun finance topic. Before we jump into the four steps to debt relief, make sure you get the free printable debt snowball worksheet bundle below so you can action the steps as you go through the example with me a little later.

Just click on the picture below for an immediate download of the free bundle:

What is the debt snowball method?

The debt snowball method is a plan that motivates you to payoff all your debt. It’s based on a snowball that grows bigger and goes faster as it gains momentum rolling down a hill.

The idea is that the snowball is your debt. You start by forming a little snowball when you pay off your smallest debt first, as quickly as possible. Then you move on to a bigger debt. But now you have more money than before because you’ve paid off one debt, so paying off the next debt is easier and goes a little quicker. Your snowball is growing in relation to your debt payments.

Once that’s paid off, the snowball continues to grow – you pay off the next debt with all the extra money from the first two debts. And so the size of the snowball grows with your increasing debt payments until all your debts are paid off.

See how the snowball gets bigger and goes faster if you follow the steps in this method?

Who should use the debt snowball method?

If you like to see quick progress and really need a boost when it comes to your debt and finances, then this is the debt payment method to choose. It’s perfect for those with many debts to pay off or those on a low income, who need a structured payment plan to pay off debt with manageable baby steps. If you follow the steps, you WILL get out of debt.

The debt snowball method is simple and easy to implement, especially if you use my free templates. You get a great sense of achievement every time a debt is crossed off that list, which motivates you to keep on going to pay off bigger debts. And that’s how your snowball grows to get you debt free!

How does debt snowball work?

In its simplest form, the debt snowball can be explained with four steps:

STEP 1: List all your debts from the smallest amount you owe to the largest. Don’t worry about the interest rates and don’t include your mortgage in this list. Continue to make the minimum payments due for all debts except the smallest one.

STEP 2: Focus on completely paying off the smallest debt first, as quickly as possible.

STEP 3: Once that debt is paid off, take the next smallest debt and pay it off as quickly as possible, adding the money you were using to pay off the previous smallest debt.

STEP 4: Rinse and repeat this process for all your debts until they are paid off.

Here’s a visual infographic of the debt snowball method, breaking it down into the four steps:

We will work through an example of the debt snowball method together using the free worksheet bundle you downloaded earlier. If you didn’t download it, you can still get it by clicking on the picture below

Debt snowball example

Here’s an example of the debt snowball method, with further explanations and tips for each step:

STEP 1: List all your debts

The definition of debt is money that you borrowed and now owe to people or institutions, like the bank. You usually agree to pay back the money over a certain period of time, often with interest.

Debts in the snowball method include any money that you owe, not your bills. So, your rent, water and other regular bills are bills, not debt (tip: look at how to bring these bills down to get that debt snowball rolling faster – the more you pay, the faster you become debt free).

Don’t include your mortgage in your debt list.

To manage your bills and your monthly finances, you need a budget like my Fun & Freedom Budget Bundle.

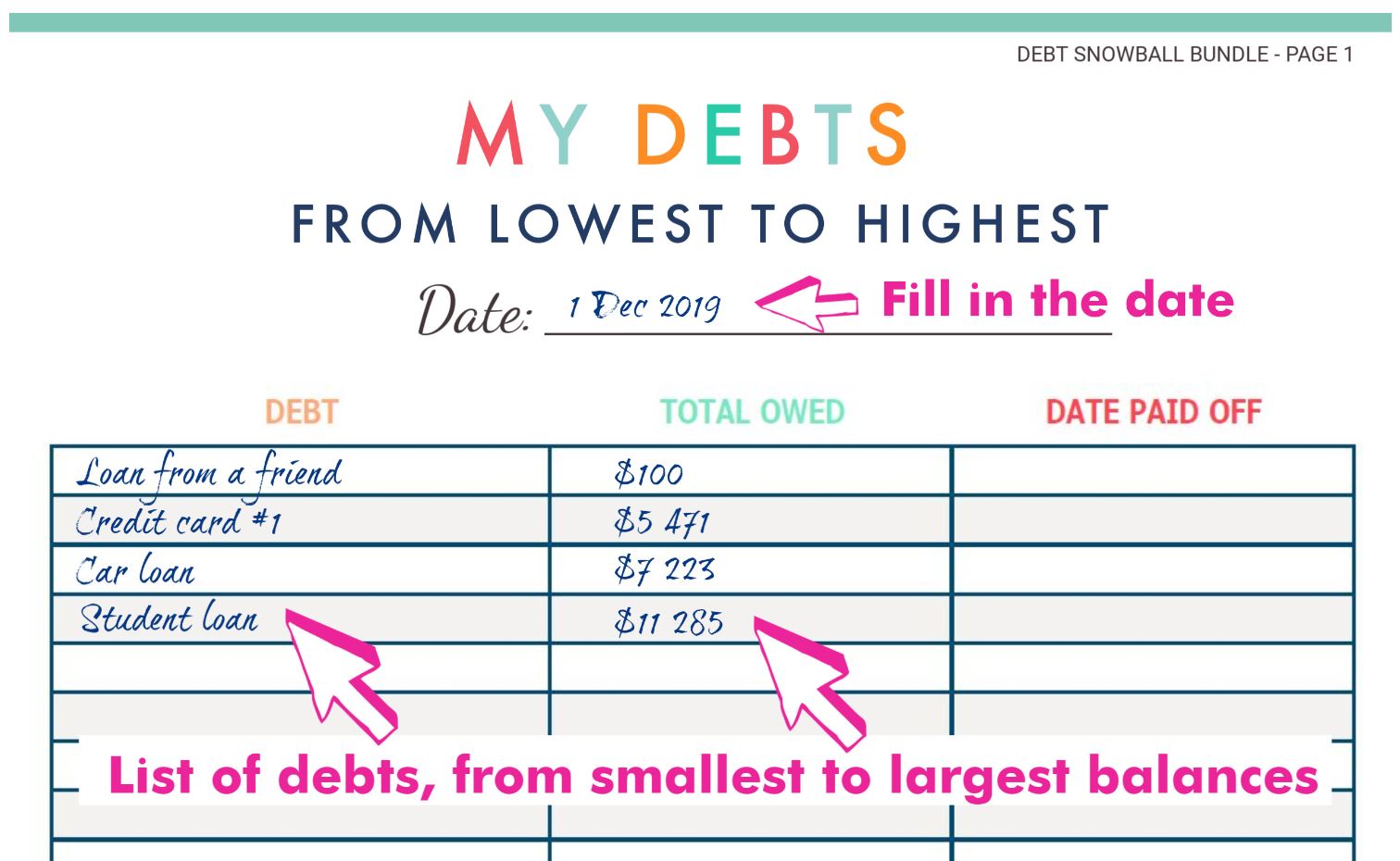

The first step in the debt snowball method is to make a list of every debt you have, including the $100 your friend lent you for that fun night out. Write down every debt you have, no matter how small it is.

You can also get a copy of your credit record to see if there are any sneaky debts you’ve forgotten about. You don’t want to miss those.

On PAGE 1 of the debt snowball worksheet, write down your list of debts in order, from the smallest balance to the highest balance:

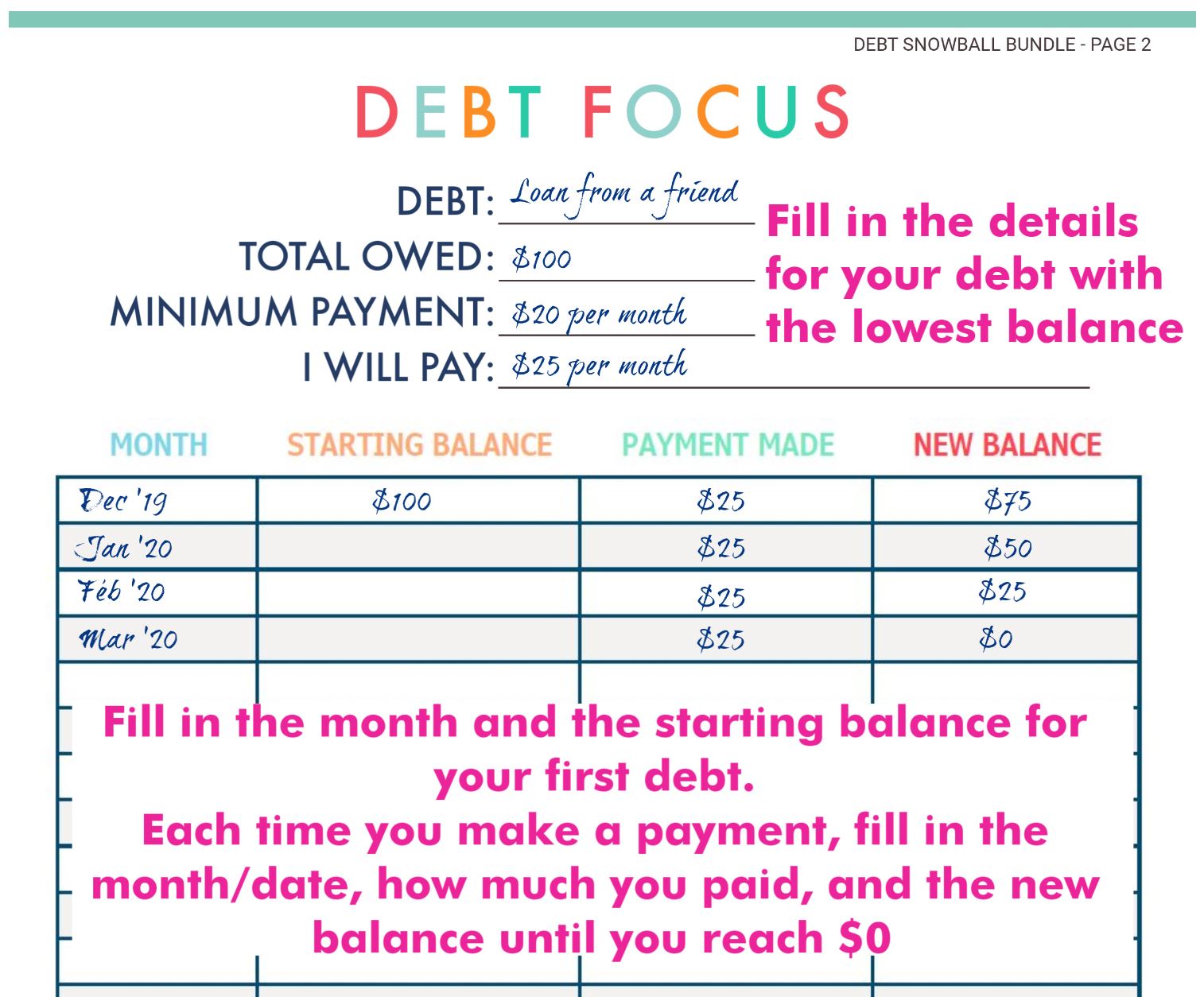

STEP 2: Pay off the smallest debt first

In step 2 you make the minimum monthly payments on all your debts and focus on paying off the smallest debt as quickly as possible (the one with the lowest balance).

Let’s go to PAGE 2 of the printable and fill in the following info for our example:

> The name of the debt

> How much you owe for that debt

> The minimum monthly payment you must make

> How much you will pay each month to crush it (the minimum monthly payment + anything extra you can afford)

Any and all extra money goes to this debt – stay focused and pay it off as quickly as you can. Find ways to bring in extra money with your hobbies and save money wherever you can, like in your budget and bringing down your monthly bills. Every single penny counts here to get that snowball rolling down the hill. Put everything you can toward paying off this debt.

Track your payments in the DEBT FOCUS spreadsheet, where you can write down each payment and the new balance for that debt.

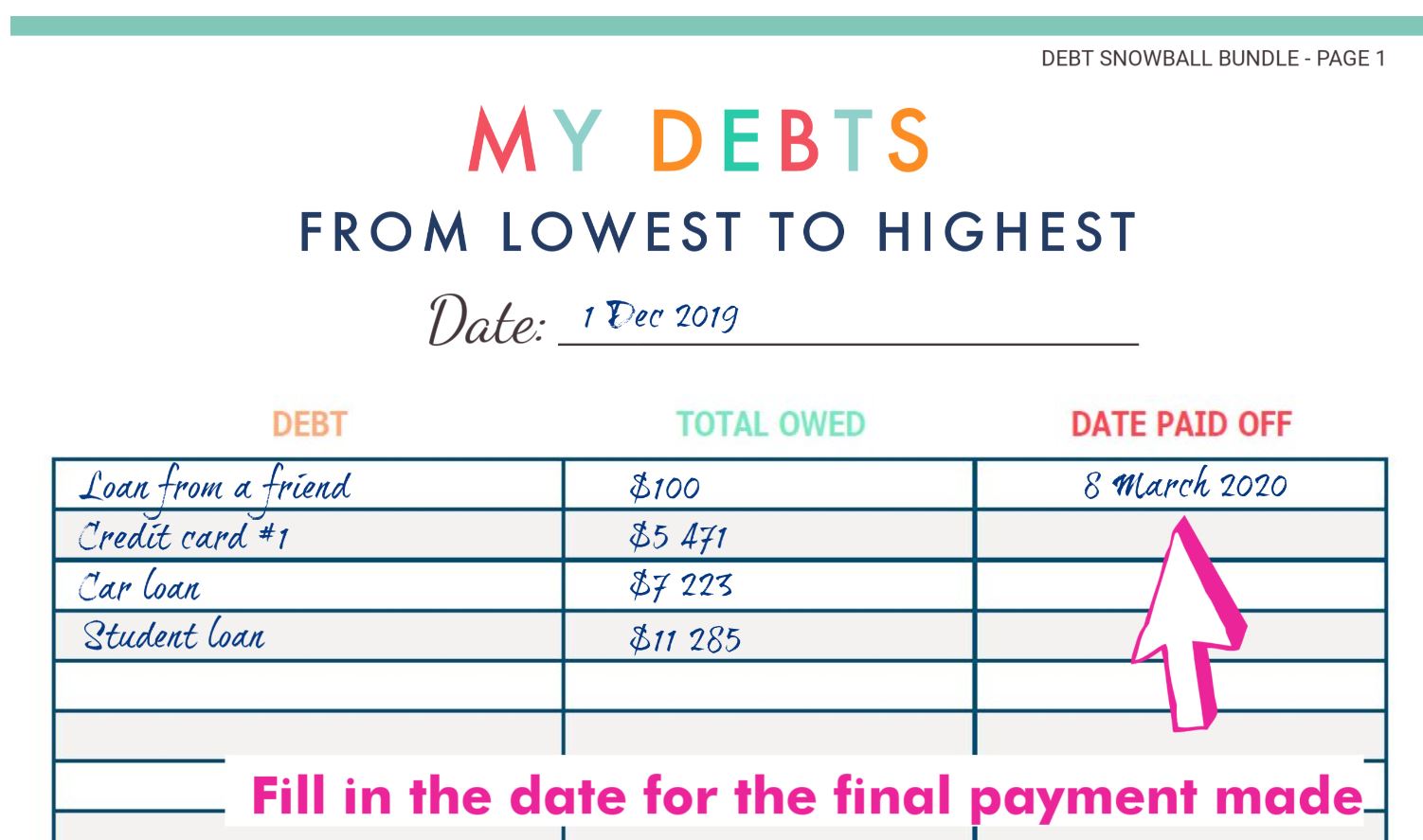

If you stay motivated and committed, this debt should be paid off pretty quickly. Fill in the date the debt is paid off in the last column of your debt list:

Now you have one less debt to worry about. You’re doing very well!

It’s time for step 3.

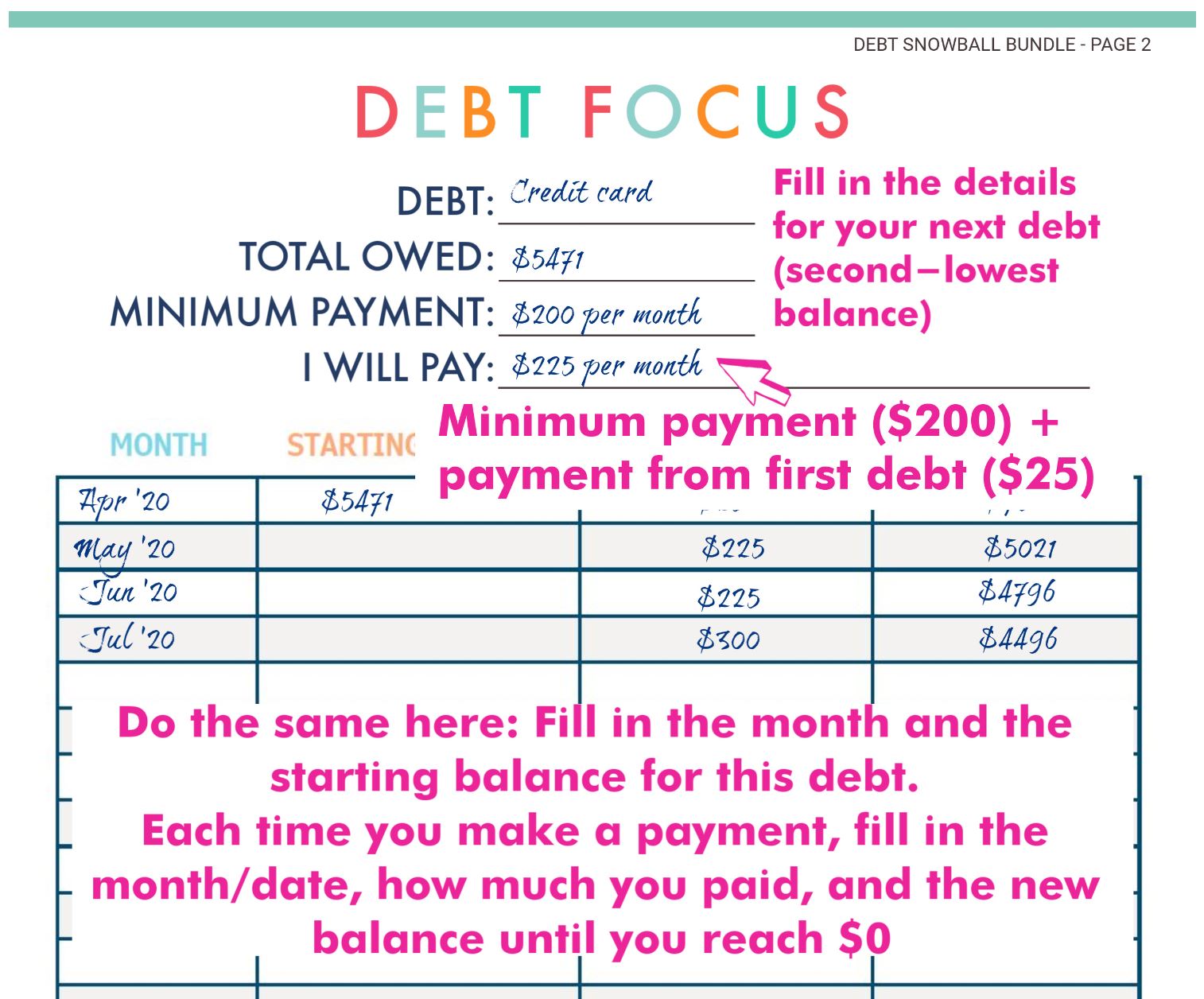

STEP 3: Start paying off the next debt

Continue making all your minimum payments on all your debts, as before. You now have a little extra money for debt payments because you paid off your first debt, right?

Print out a new DEBT FOCUS sheet and fill it in with the next smallest debt on your list, the one with the second-lowest balance. Start paying off that debt with the minimum monthly payment + the extra money you have from paying off the first bill + any more money you can make.

Keep going until it’s paid off. Fill in the date you pay it off in your list of debts. That snowball should be rolling nicely now.

STEP 4: Keep paying off the next debt

Now start on your debt with the third-lowest balance, paying the minimum monthly payment + money from paying off the first and second bills + any extra income you can bring in.

Continue paying the minimum monthly payments on the rest of your debts so you don’t fall behind with anything.

Keep on going until all your debts are paid off, so the snowball rolls to the end and you are blissfully debt-free.

Every time you pay off a debt, you take that debt’s minimum monthly payment and roll it over to pay off the next debt, adding any extra money that you can earn that month.

FAQs about the debt snowball method

Is the debt snowball a good idea?

Yes, the debt snowball method is a great idea for debt relief. You get to manage your debts with a worksheet, which keeps you motivated with how to pay off debt. And the more you pay off, the easier it gets to become totally debt free.

Is the snowball or avalanche method better?

The snowball method is better if you need a quick win and you have many debts to pay off. You will see faster results with the debt snowball method.

What does debt snowball mean?

Debt snowball means paying off all your debt in 4 steps. The snowball represents your debt payments. Each time you pay a debt, you put that money to pay off the next debt, making your payments higher (and debt lower). Your snowball grows with your debt payments and gets momentum along the way to pay off debts faster.

Should I pay off smallest debt first?

Yes, if you’re struggling with money then pay off the smallest debt first. This will give you some relief and free up some money to pay the next debt. You can use the debt snowball method worksheet to plan your payments and track your progress as you get out of debt.

Grab the free debt snowball worksheet bundle

Here’s your last chance to get the free debt snowball worksheet bundle to help you pay off your debt:

Conclusion

The debt snowball method is an easy, 4-step process to pay off all your debt. If you follow these steps and stick to your payments, then you will become debt-free. I hope these gorgeous free debt snowball templates inspire you to take this big step to financial freedom!

Now that you’re busy paying off debt, avoid getting into any more bad debt. You could try this easy 52-week saving challenge to save over $1000! Or get The Fun & Freedom Budget Bundle to help you manage your money, including your bills. If you’ve been under a lot of pressure and are not feeling yourself these days, you could check out the symptoms of burnout and how to recover from it.